Impact of Goods and Services Tax on the Economic Growth of India

March 2024 | Swathy Krishna and Shacheendran V

Abstract

An efficient tax system is vital for the sustainable growth of the nation. In India, indirect taxes constitute major portion of the tax revenues for balancing government budgets. During last few decades Value Added Tax has been seen as a leading income generating source. After prolonged discussions India adopted a comprehensive Goods and Services Tax, which aimed at the removal of cascading effect of taxes through seamless availing of input tax credit. The present paper is an attempt to find empirical evidence on the relationship between Goods and Services Tax revenue growth and economic growth proxy by GDP. The ordinary least square regression technique found that GST revenue growth has a significant and positive impact on economic growth in India during the period Q2:2017 to Q1:2021. The result shows that one per cent GST revenue growth causes 0.56 per cent economic growth. The result of correlation analysis also confirms the association between GST revenue performance and economic growth.

Key Words

Economic growth, Goods and services tax, Gross domestic product.

I Introduction

Structure of tax system has been gaining attention due to the immense impact on social, political and economic system. An efficient fiscal system can mobilise adequate financial resources to attain equilibrium growth of the economy (Munir and Riaz 2019). In India, indirect tax revenue constitutes more than 50 per cent of the total tax revenue collection, thus playing a vital role in mobilising funds for public expenditure. Many of the developing countries are facing difficulties to satisfy their revenue requirements; and it has been found that an effective tax administration and positive public perception on tax management can improve tax compliance (Mawejje and Sebudde 2019). In this globalised era, countries across the globe are incorporating various structural and fiscal reforms to enhance the tax potential. Value Added Tax (VAT) is considered to a superior method among the indirect taxes (James 2011), at present more than 160 countries follow value addition-based taxing mechanism. Sophisticated IT based Value Added Tax system is found to be the best taxing method with a capability of processing vast amount of data (Abd-Mansor, Mohamed, Ling, and Kasim 2016). An effectual fiscal reform could achieve optimised economic growth (Ma and Mao 2016). Fiscal reforms and its role on economic growth have been gaining more attention from the policy makers and other academicians. A well-established fiscal policy can become an economic recovery tool (Mundell 2012), fiscal reforms could improve the propensity to save and can accelerate the rate of capital formation. Economist believes that there is a strong relationship between tax reforms and economic growth, but there are also studies which found conflicting findings about the relationship between taxation and economic growth (Landau 1986, Loganathan, Shahbaz, and Taha 2014, Onakoya and Afintinni 2016, Al-Tarawneh, Khataybeh, and Alkhawaldeh 2020), thus creating a need for further exploration about the two variables.

The study is structured as follows: In Section II, we provide a brief description about tax revenue performance of the Indian economy over the study period. Section III describes the literature review that includes previous studies related to revenue analysis and forecasting. Section IV whichdeals with the research methodology and followed by the empirical results of the study, in Section V. The study made an attempt to draw some policy conclusion in Section VI.

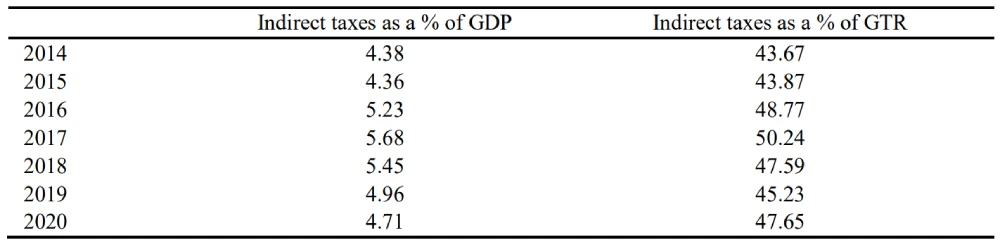

II Tax Revenue Performance

Tax is the major revenue contributor at all the tiers of the government, and tax revenue constitutes the receipts from direct and the indirect taxes. The Indian GST came into existence by subsuming about 17 previously levied indirect taxes namely services tax, excise duty, value added tax, central sales tax, entertainment tax, and entry tax. As per the recommendation of the GST Council, specific petroleum products and alcoholic liquor for human consumption are kept outside the levy of GST; these products being a major revenue source for the States, converging the existing levies on such products to GST will have a significant impact of the revenue performance of the States. Thus, these products are taxed in the same manner as under the pre-GST regime.

Table 1: Indirect Taxes Contribution

Sources: Computed based on Comptroller and Auditor General Report.

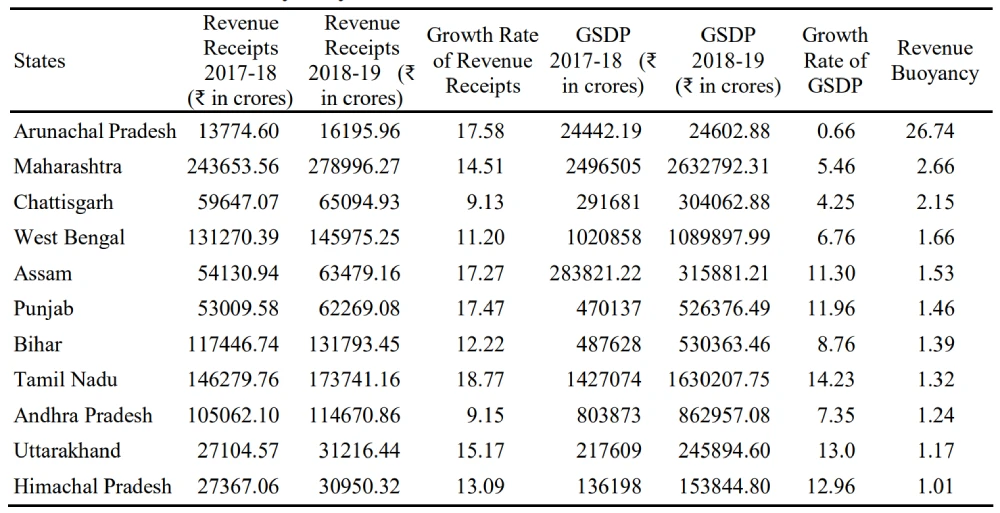

Efficient tax reform ensures optimum revenue mobilisation; increased government expenditure created a need for raising additional revenues especially in case of developing countries. Tax systems across the globe have been facing different forms of revision and restructuring to enhance the efficiency of revenue mobilisation. Tax buoyancy measures the revenue efficiency, as it measures the responsiveness of change in tax revenue to the change in the GDP. Higher tax buoyancy indicates an increased share in tax revenue in the total GDP, indicating administrative efficiency (Mawia and Nzomol 2013).

Table 2: Revenue Buoyancy for 2018-19

Source: Comptroller and Auditor General Report (2018-19).

III Literature Review

Studies concerning macroeconomic impact of fiscal policy have been gaining more attention due to revenue inadequacies and increased external borrowings. Numerous studies tried using time series and other theoretical model to examine the macroeconomic impact of tax reforms. Hayo and Uhl (2014) used Blachard and Perotti developed VAR model to study the macroeconomic impact of tax change in Germany using the variables namely output, taxes, government expenditure, inflation and short-term interest rate. The result shows a significant decline in the output level due to policy change and a point change in the tax-to- GDP ratio can reduce the output by 2.4 per cent.

Castro (2006) analysed the fiscal shock on GDP, prices and interest rates in Spain using Vector Autoregressive Model. The result showed the government expenditure shows negative response toward output, private consumption and investment in the medium run. Moreover, the expenditure shock led to higher prices and interest rate. The study confirms that in short run the increased taxes can improve the GDP, consumption and investment through effective management of public expenditure. Madsen and Damania (1996) tried to measure the impact of fiscal structural change on wage and output levels using PRS analysing performed on the basis of Engle-Yoo (1989) procedures. The panel study was conducted among 22 OECD countries using time series data from 1960-1990, the study found in short run the tax changes led to increased output level, while in long run an opposite can be observed in majority of cases. Munir and Riaz (2019) tried to explore the relevance of planned fiscal policy for building a stable microeconomic environment. The study used VAR model to analyse the macroeconomic consequence of fiscal policy in Pakistan using quarterly time series data for the period 1976 to 2017. The result of the study found that prices do not respond to increase in government expenditure, which increase in taxes cause immediate response in prices.

Munir and Riaz (2019) studied the influence of fiscal policy on GDP, private consumption, private investment, prices and interest rate in Pakistan using Vector Auto Regressive model. The examination of macroeconomic effect found that increase in government expenditure can improve the GDP, further it was also identified that increase in total taxes lead to a positive increase in GDP. A comparative study on the macroeconomic effect of adopting GST was conducted by Bolton and Dollery and found a neutral tax design will have a negligible impact on the economy, economic efficiency is to be obtained by a broadened tax-based system. The study also highlights that the relative economic performance showed varied impact due to GST adoption across the three countries i.e., Australia, Canada and New Zealand.

A well-structured tax system could act as mediator for economic growth, through efficient mobilisation of resources and improving standard of living of the people. Value Added Tax mechanism is considered to be a more effective taxing mechanism due to revenue neutrality, revenue efficiency, simplicity and equity. There are a number of empirical studies trying to investigate the relationship between VAT and economic growth.

Hassan (2015) used OLS regression method to examine the impact of VAT on economic growth in Pakistan, using time series annual data for the period 1991- 1992 to 2011-2012. The econometric analysis found a significant and positive impact of tax revenue on the nominal GDP, indicating the relationship between tax revenue and economic growth. The result shows an increase in one per cent of the VAT revenue causes 0.24 per cent increase in the economic growth. Basila (2010) tried to explore the role of VAT as an economic development tool in Nigeria. The econometric analysis found strong and positive correlation between VAT and GDP; thus, the study confirms that a good planned and implemented tax system could bring balance economic development through efficient revenue performance. Similarly, in the study conducted by Onwuchekwa and Aruwa (2014) found the VAT revenue plays a significant role in economic development of Nigerian economy, through their contribution towards total government revenue.

A number of empirical studies have found a significant relationship between tax revenue and economic growth, but there are also studies which found contrasting result. Michael and Lockwood (2010) conducted a panel study among 143 countries over the period of 25 years, which tried to explore impact of VAT on revenue performance. The empirical analysis shows inconsistent result regarding VAT impact on the economies. In majority of the cases the VAT adoption found to improve the overall revenue- to GDP ratio, while there are also situations where the system led to overall negative impact on the economies. International experience shows a significant decline in the Government revenue as a percentage of GDP during the initial phase of GST implementation (Bolton and Dollary 2010).

Leemput and Wiencek (2017) tried to analyse the welfare impact of tax reform on Indian economy, the estimated impact of GST under the baseline scenario with a standard tax rate of 16 per cent was found to increase the welfare effect by 5.3 per cent. The domestic and internationaltrade is expected to increase by 29 per cent and 32 per cent respectively, furthermore, the static model found consistent welfare impact was found across different States in India.

IV Data and Methodology

Data

The following study carried out an empirical analysis using quarterly time series data for the period Q2:2017 to Q1:2021. The time series data on GDP were obtained from database of Reserve Bank of India (RBI) and the Press Release of Ministry of Statistics and Programme Implementation, and the data on GST revenue was obtained from the Press Release of Department of Revenue, Ministry of Finance. The data of GDP and GST revenue is expressed as the percentage growth. The study used least square regression technique to study the relationship between GST revenue growth and Economic Growth using the proxy variable GDP.

Model Specification

The study tried to examine the impact of GST revenue growth, i.e., the independent variable on the dependent variable economic growth (GDP). The study used the following model specification to investigate the relationship between the dependent and the independent variable.

GDP = b0 + b1(GST) + e

where

GDP Gross Domestic Product (per cent growth)

GST Goods and Services Tax Revenue (per cent growth)

b0 is the intercept of the model, and b1 is the regression coefficient and e is the error term.

V Empirical Results

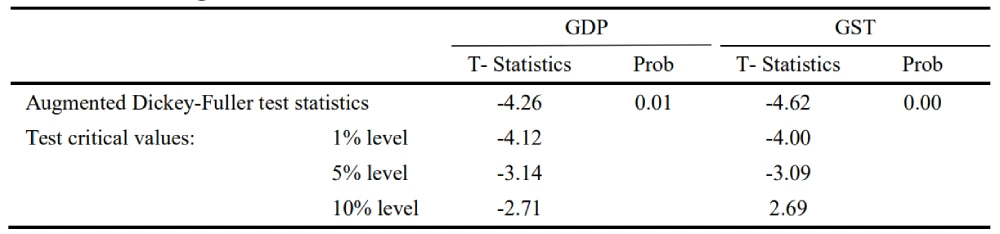

Unit Root Test

The time series data may be affected by trend with passage of time, the unit root test ensures the presence or absence of stationarity in the data set. Presence of stationarity validates the standard hypothesis test; thus, it is significant to test the unit root of the data using appropriate test.

Table 3: Testing of Unit Root

Source: Computed using e-views.

Augmented Dickey-Fuller test was used to check the presence or absence of stationarity in the time series data; the unit root represents the non-stationarity of the data. Since the p value of the variable GDP growth were found to be lesser than 0.05, the null hypothesis that the series has unit root is rejected. Thus, indicating stationarity of GDP growth at the level itself. The variable GST revenue growth became stationary at the level itself with a p value less than 0.05, making the data suitable for further statistical analysis.

Testing of Normality

Testing of normality is a prerequisite for performing least square regression analysis to study the relationship between the independent and dependent variable. The study used Jarque – Bera test to find out the normality of the residuals. The Jarque – Bera test uses the sample kurtosis and sample skewness to measure whether the distribution is normal or not so.

Table 4: Testing of Normality

Source: Computed using e-views.

The Jarque – Bera test found the p value greater than 0.05, thus the null hypothesis is accepted that residuals follow a normal distribution.

Autocorrelation and heteroskedasticity

The diagnostic test results related to checking serial correlation and heteroskedasticity are shown in Table 5. The Breusch – Godfrey Serial Correlation LM test shows f-statistics of 0.39, observed *R of 1.00 and probability value of 0.61. The result indicates that the probability value of 0.61 is greater than 0.05 critical value, thus indicating that the model is free from the presence of serial correlation. The study used Breusch-Pagan-Godfrey test to measure heteroskedasticity, the test shows f-statistics of 3.64, observed *R of 3.28 and probability value of 0.07. The results indicate that the probability value of 0.07 is greater than 0.05 critical value, thus the hypothesis the residuals are having homoscedasticity is accepted

Table 5: Testing of Autocorrelation and Heteroskedasticity

Source: Computed using e-views.

Correlation

The study uses Karl Pearson correlation coefficient to investigate the direction of relation between the dependent variable and the independent variable. The result shows that the variable economic growth has a strong relationship with GST revenue growth with a correlation coefficient of 0.86.

Table 6: Correlation Analysis

Source: Computed using e-views.

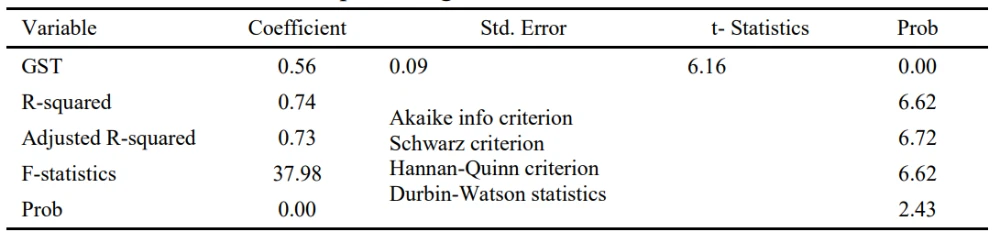

Table 7: Results of Least Square Regression Method

Notes: Dependent Variable: GDP; Method: Least Square; Included Observation:15.

Source: Computed using e-views.

The above Table 7, shows a R-square value of 0.74 indicating that the 74 per cent of the change in the dependent variable (GDP growth) has been explained due to the changes in the independent variable (GST growth). Similarly, the adjusted R-squared value of .73 can considered to be very good for forecasting. The analysis found that GST revenue growth has a positive and significant impact on GDP growth in India for the post GST period, with a p-value less than 0.05. The results indicate that one per cent GST revenue growth causes 0.56 per cent economic growth, corroborates the strong and positive relationship between GST revenue growth and economic growth (GDP).

VI Conclusion

The paper attempts to find empericial evidence on the impact of GST revenue growth on the economic growth of India using the time series data for the period 2017-2021. The relationship between GST revenue growth and economy growth is performed through stationarity test, i.e., Augmented Dickey-Fuller test, wherein the variables are found to be stationaryat the level. The Ordinary Least Square Regression techniques found significant and positive impact of GST revenue growth on economic growth in India. The empirical finding of the study is consistent with the result of the studies Hassan (2015), Akhor and Oshoke (2016), Gatawa, Aliero, and Aishatu (2016), Erero (2021). The result of the study corroborates the need of strengthening the tax system for enhancing the tax revenue performance, enabling the economic system to have better tax enforcement for improving tax compliance.

The main limitation of the present paper is that it has not analysed the other factors influencing the GDP growth with respect to the Indian economy. The second, that the study was primarily based on secondary data collected and compiled by various government organisations.

Affiliation

Swathy Krishna, Junior Research Fellow, Department of Management Studies, Kannur University,

Palayad, Kannur District 670661, Kerala, Email: swathykrishnaek@gmail.com,

Contact No. 8848309153

Shacheendran V, Associate Professor, GPM Govt. College, Manjeshwaram, Kasaragod District

671323, Kerala, Email: shachica@rediffmail.com, Contact No. 9497292772

References

Abd-Mansor, N.H., I.S. Mohamed, L.M. Ling, and N. Kasim (2016), Information Technology Sophistication and Goods and Services Tax in Malaysia, Procedia Economics and Finance, 35(1): 2-9, https://doi.org/10.1016/S2212-5671(16)00003-4

Akhor, S.O. and O.U. Ekundayo (2016), The Impact of Indirect Tax Revenue on Economic Growth: The Nigeria Experience, Igbinedion University Journal of Accounting, 2(08): 62-87.

Al-tarawneh, A., M. Khataybeh and S. Alkhawaldeh (2020), Impact of Taxation on Economic Growth in an Emerging Country, International Journal of Business and Economics Research, 9(2): 73-77, https://doi.org/10.11648/j.ijber.20200902.13

Basila, D. (2010), Investigating the Relationship between VAT and GDP in Nigerian Economy, Journal of Management and Corporate Governance, 2(2): 65, 72.

Bolton, T. and B. Dollery (2010), An Empirical Note on the Comparative Macroeconomic Effects of the GST in Australia, Canada and New Zealand, Economic Papers: A Journal of Applied Economics and Policy, 24(1): 50-60, https://doi.org/10.1111/j.1759-3441.2005.tb00994.x

De Castro, F. (2006), The Macroeconomic Effects of Fiscal Policy in Spain, Applied Economics, 38(8): 913-924, https://doi.org/10.1080/00036840500369225

Erero, J.L. (2021), Contribution of VAT to Economic Growth: A Dynamic CGE Analysis, Journal of Economics and Management, 43(1): 26-55.

Gatawa, N.M., H.M. Aliero and A.M. Aishatu (2016), Evaluating the Impact of Value Added Tax on the Economic Growth of Nigeria, Journal of Accounting and Taxation, 8(6): 59-65, https://doi.org/10.5897/JAT2016.0226

Hassan, B. (2015), The Role of Value Added Tax in the Economic Growth of Pakistan, International Journal of Public Policy, 11(4-6): 204-218, https://doi.org/10.1504/IJPP.2015.070554

Hayo, B. and M. Uhl (2014), The Macroeconomic Effects of Legislated Tax Changes in Germany, Oxford Economic Papers, 66(2): 397-418, https://doi.org/10.1093/oep/gpt017

James, K. (2011), Exploring the Origins and Global Rise of VAT, The VAT Reader (Tax Analysts), 1(1), 15-22. doi.org/10.2139/ssrn.2291281

Keen, M. and B. Lockwood (2010), The Value Added Tax: Its Causes and Consequences, Journal of Development Economics, 92(2): 138-151.

Landau, D. (1986), Government and Economic Growth in the Less Developed Countries: An Empirical Study for 1960-1980, Economic Development and Cultural Change, 35(1): 35-75, https://doi.org/10.1086/451572

Loganathan, N., M. Shahbaz and R. Taha (2014), The Link between Green Taxation and Economic Growth on CO2 Emissions: Fresh Evidence from Malaysia, Renewable and Sustainable Energy Reviews, 38 (issue no): 1083-1091, https://doi.org/10.1016/j.rser.2014.07.057

Ma, G. and J. Mao (2018), Fiscal Decentralisation and Local Economic Growth: Evidence from a Fiscal Reform in China, Fiscal Studies, 39(1): 159-187, https://doi.org/10.1111/j.1475- 5890.2017.12148

Madsen, J. and D. Damania (1996), The Macroeconomic Effects of a Switch from Direct to Indirect Taxes: An Empirical Assessment, Scottish Journal of Political Economy, 43(5): 566-578, https://doi.org/10.1111/j.1467-9485.1996.tb00951.x

Mawejje, J. and R.K. Sebudde (2019), Tax Revenue Potential and Effort: Worldwide Estimates Using a New Dataset, Economic Analysis and Policy, 63(C): 119-129, https://doi.org/10.1016/ j.eap.2019.05.005

Mawia, M. and J. Nzomoi (2013), An Empirical Investigation of Tax Buoyancy in Kenya, African Journal of Business Management, 7(40): 4233-4246, https://doi.org/10.5897/AJBM2013.7212

Mundell, R. (2012), The European Fiscal Reform and the Plight of the Euro, Global Finance Journal, 23(2), 65-76. https://doi.org/10.1016/j.gfj.2011.10.009

Munir, K., and N. Riaz (2019), Macroeconomic Effects of Fiscal Policy in Pakistan: A Disaggregate analysis, Applied Economics, 51(52): 5652-5662, https://doi.org/10.1080/00036846.2019. 1616074

Onakoya, A.B. and O. I. Afintinni (2016), Taxation and Economic Growth in Nigeria, Asian Journal of Economic Modelling, 4(4): 199-210, https://doi.org/10.18488/ 8/2016.4.4/8.4.199.210

Onwuchekwa, J.C. and S.A. Aruwa (2014), Value Added Tax and Economic Growth in Nigeria, European Journal of Accounting Auditing and Finance Research, 2(8): 62-69.

Van Leemput, E. and E.A. Wiencek (2017), The Effect of the GST on Indian Growth, Board of Governors of the United States Federal Reserve System, International Finance Discussion Paper Note.